Navigating today’s financial landscape is tough for everyone, but recent research highlights a concerning trend for Gen Z. They are confronting formidable hurdles in securing their financial future. With mounting student loans, soaring housing market rates, and the relentless impact of inflation, Gen Z finds themselves accumulating debt while striving to maintain a certain lifestyle, and they’re using credit cards to bridge the gap.

Evidence suggests that inadequate financial education could be an underlying cause of Gen Z’s debt dilemma. Empowering them with the right tools is key to tackling a rising challenge and positions your credit union as a standout choice for the Gen Z audience.

The Debt Dilemma

Gen Z is adopting credit cards at an unprecedented rate. According to TransUnion, their credit card usage is surpassing that of their predecessor, the Millennials, despite only half of Gen Z being old enough to use credit.

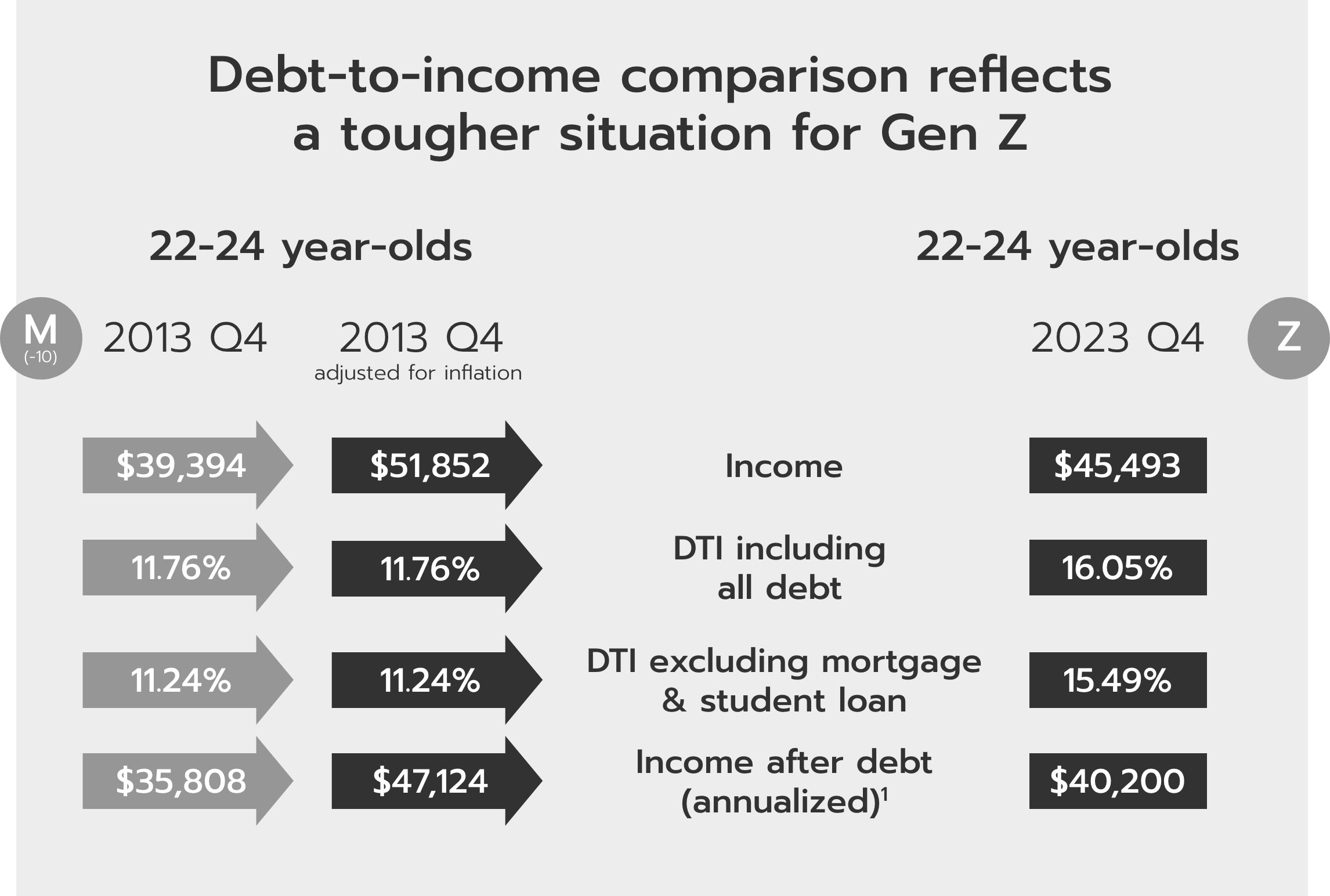

Although relying on credit cards to cover expenses isn’t exclusive to Gen Z (outstanding credit card balances exceed $1 trillion post-pandemic), the issue is exaggerated for this generation. Even when accounting for inflation, Gen Z’s average year-end balance owed is significantly higher (26%) than that of Millennials at the same age.

1. Income after debt is annualized and computed as the difference of the monthly gross income and the total minimum payment due. Calculations exclude rental and utilities debt for all consumers.

THE FINANCIAL BRAND © May 2024

SOURCE: TransUnion Consumer Credit Database | Bureau of Labor Statistics (BLS)

Researchers suggest that the difference in Gen Z’s credit card usage stems from their unique economic experiences. Millennials were significantly influenced by the Great Recession during their formative years, which likely influenced their approach to debt. In contrast, Gen Z encountered economic challenges like the COVID-19 pandemic and subsequent inflation as they gained financial independence.

The Solution

Given the persistent financial challenges facing Gen Z, credit unions have a prime opportunity to attract a younger audience by helping pave the way to a more secure financial future.

The key to attracting Gen Z is to offer technology-based financial education resources. This generation highly values both technology and convenience, making digital financial education an effective way to engage them and guide them towards financial security.

Gen Z perceives credit unions as lagging in digital offerings, which can be a deterrent. It’s crucial to evaluate your current strategy and focus on enhancing digital services to attract and engage this younger demographic.

Consider the following:

-

Financial

literacy webinars -

Budgeting

eCourses -

Online

assessments -

Video conferences

with advisors

-

Online

communities -

Podcasts

-

Social

media content

To support Gen Z’s positive financial behaviors, consider implementing a rewards program. Rewarding their actions not only motivates them to stay on track but also strengthens their loyalty to your institution. This strategy is effective in fostering financially healthy, life-long members.

The Bottom Line

Addressing Gen Z’s financial challenges requires a strategic approach that aligns with their technological preferences and lifestyle needs. By integrating tech-driven financial education into your offerings and rewarding positive financial behaviors, credit unions can help mitigate this generation’s debt dilemma and position themselves as the go-to financial partner for young members.

Ready to help Gen Z with the debt dilemma?

At RAZR Financial, We strive to achieve a common understanding of how to solve the business challenge and what strategy to use going forward.

Reach out to learn more about RAZR Financials’ strategic consulting services.